This is part six in an ongoing series. Prior posts are available here:

- Part 1 covered GMV trends from Jan 1 – Mar 17, 2020

- Part 2 covered GMV trends from Jan 1 – Mar 22, 2020

- Part 3 covered GMV trends from Jan 1 – Mar 31, 2020

- Part 4 covered GMV trends from Jan 1 – Apr 12, 2020

- Part 5 covered GMV trends from Jan 1 – Apr 20, 2020

The last time we posted, we were in the middle of what we called the “stimulus bump.” This post looks at GMV trends through the end of April and the first several days of May to see if that specific trend continued.

As a reminder, because there are so many changes on a daily basis, we’ve built a COVID-19 resources page to help you keep up with major developments in e-commerce. This blog post is designed to provide an update on Rithum aggregate gross merchandise value (GMV) trends.

First, some important points to understand before digging into the data:

- This data is based on marketplaces GMV aggregated across our entire customer base globally and compares Jan 1 – May 5, 2019 against Jan 1 – May 4, 2020. The final dates are offset by one day due to leap year.

- The data presented below highlights only specific marketplace categories, which are merely a subset of all categories. Because marketplaces have different category structures, the data is presented using categories that have been standardized by Rithum.

- This data is not a proxy for overall e-commerce activity or the performance of any individual business, including Rithum or any individual marketplace.

- The data shown below is based on a year-over-year comparison of trailing 7-day GMV and is expressed as percentage growth, but with actual numbers removed. The Y-axis scale is different on each graph.

- All calculations are done in USD. Global currencies are converted to USD using the conversion rate on the day of the order. These results are not normalized to account for fluctuating exchange rates. Please note that there has been significant volatility in various currencies, such as GBP, which may impact these trends.

Now, let’s see what happened to the stimulus bump.

The Stimulus Bump: Epilogue?

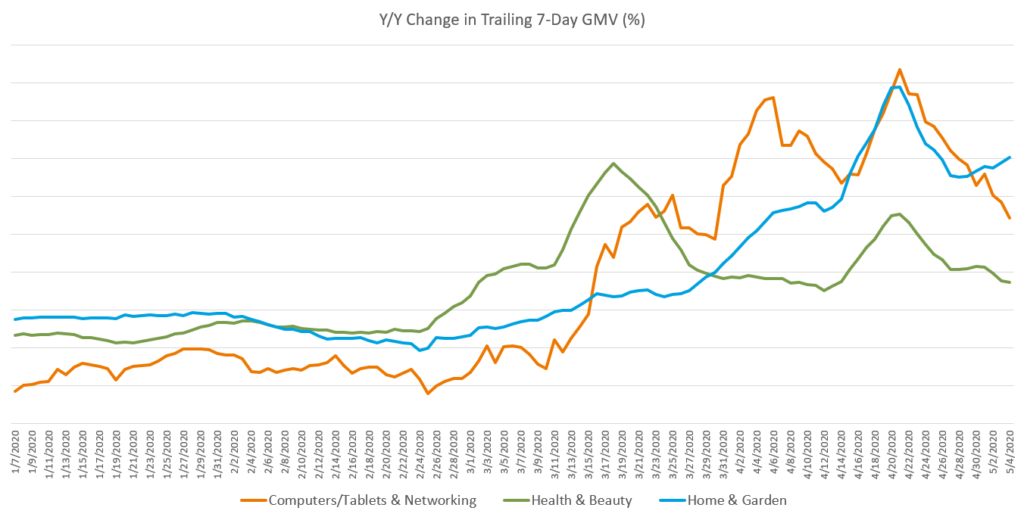

Three top-level categories that we have consistently highlighted in this series include “computers/networking”, “health and beauty”, and “home and garden.” These have been three of the higher-performing categories since mid-March. In mid-April, about the time the stimulus payments arrived in the United States, we saw an increase in year-over-year growth rates in each of these categories, though not quite as much in health and beauty. The increasing growth rates continued until around Apr 21 and then, as expected, started their inevitable decline. However, growth in these categories still remains strong relative to the growth rates seen earlier in 2020.

One thing to note is that Apr 19-21 was Easter weekend in 2019. Thus, year-over-year growth rates on these days benefited from favorable comps in addition to the impact of the stimulus payments in the United States. This trend is also moderately apparent in reverse. Apr 10-12 (Easter weekend 2020) had a slight dip in growth rates versus the unfavorable comp from 2019.

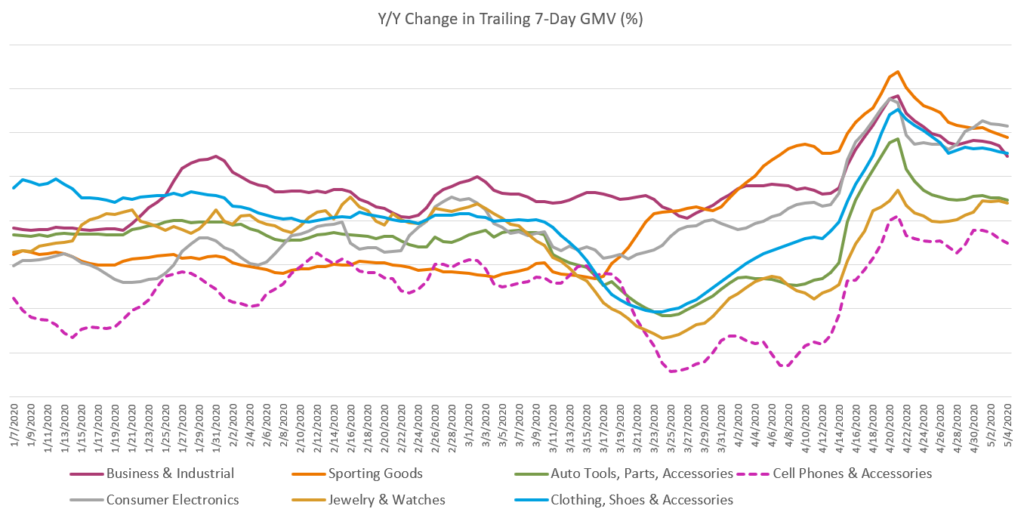

We saw very similar trends in the other categories highlighted in the last post. GMV spiked around the time the majority of U.S. stimulus payments arrived. Despite recent declines, year-over-year growth rates remained strong.

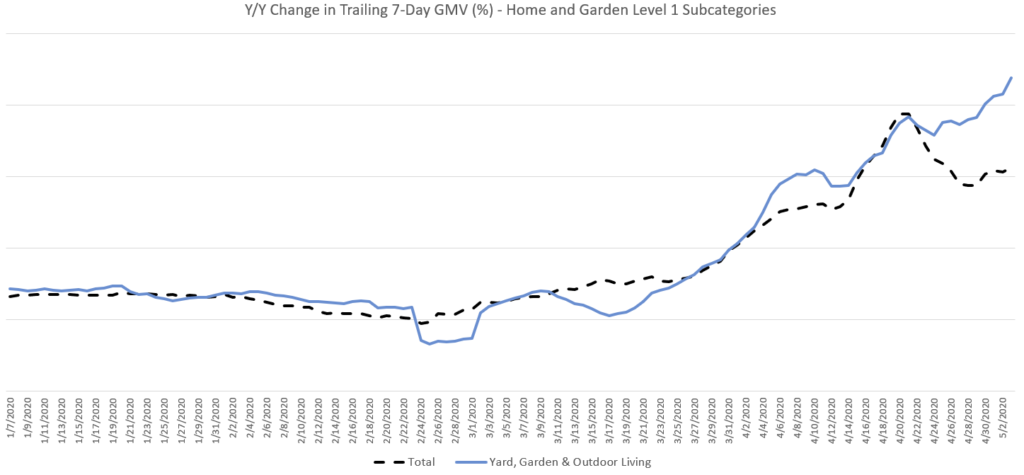

Home and Garden

In previous posts, we also tracked the strength of many deeper-level subcategories, since the growth of those subcategories illustrated key industry trends. Sometimes that subcategory growth helped drive growth rates in the top-level category, and sometimes it represented an outlier.

In the following section, we’ll be taking a step up from those deeper-level subcategories to focus on a subset of “level 1” subcategories (e.g., “yard, garden, outdoor living,” which is one level down from the top-level category of “home and garden”), so that broader trends can be observed. In the next section, we only compare sales from sellers that were active in the “home and garden” category in both 2019 and 2020.

Moving forward, we’ll refer to these level 1 subcategories as “L1Cats”.

Yard, Garden, Outdoor Living

As we noted in the last post, the “home and garden” category has been a strong performer since the latter part of March. In part 2 of this series, we highlighted strength in the subcategories of cleaning products, desks/home office, and coffee pods/K-cups.

The largest L1Cat is “yard, garden, outdoor living.” With some exceptions, including the last week or so, this L1Cat has tracked in-line with the overall home and garden category year-to-date.

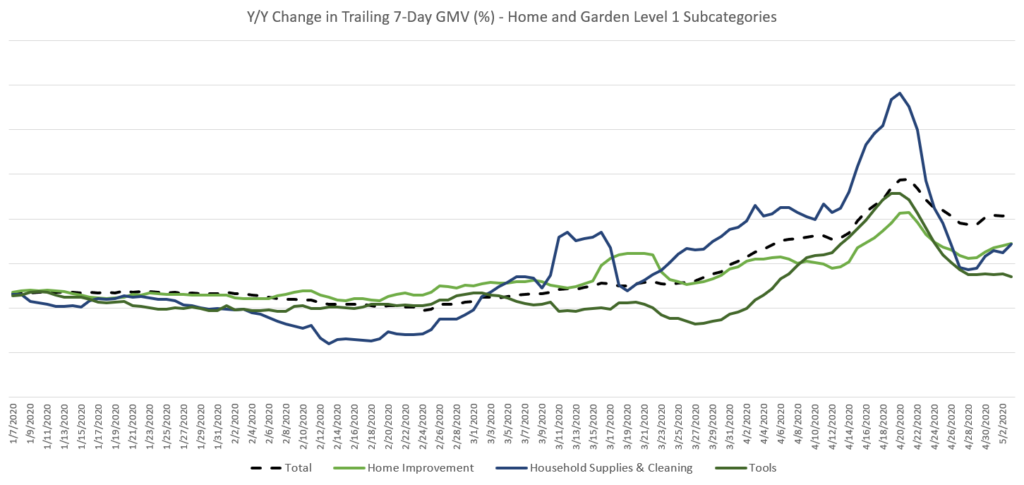

Home Improvement, Household Supplies, Tools

In prior posts, we discussed the spike in sales of cleaning supplies as consumers prepared for the COVID-19 pandemic. Cleaning supplies fall into the larger L1Cat of “household supplies and cleaning,” which also includes vacuums, carpet care, laundry supplies, brooms, mops, and more. This L1Cat has outperformed the overall category until the last week but, like most of the L1Cats, still has higher year-over-year growth rates than earlier in 2020.

The tools and home improvement L1Cats were relatively steady, although they saw a dip at the end of March when consumer spending declined, followed by growth as consumers began to leverage e-commerce more during the “lockdown.”

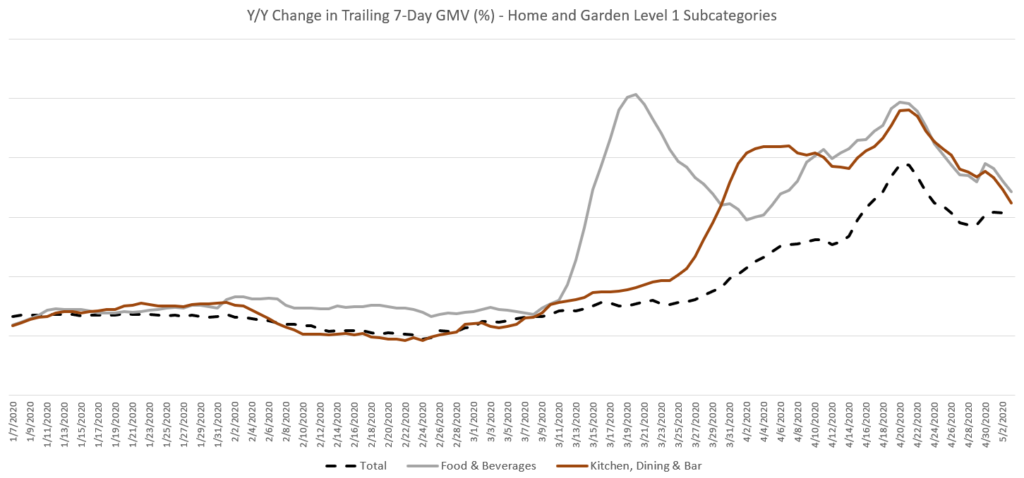

Food & Beverages, Kitchen & Dining

One L1Cat we have not mentioned in prior posts is “food and beverages,” which had relatively steady year-over-year growth until mid-March, when more consumers found themselves at home and began placing more food orders online. “Kitchen, dining, and bar” — which includes items like small kitchen appliances, kitchen gadgets, bar accessories, cookware, baking accessories, dinnerware, cutlery, linens, and more — also had relatively steady growth until late March, when it began to quickly outpace early 2020 results.

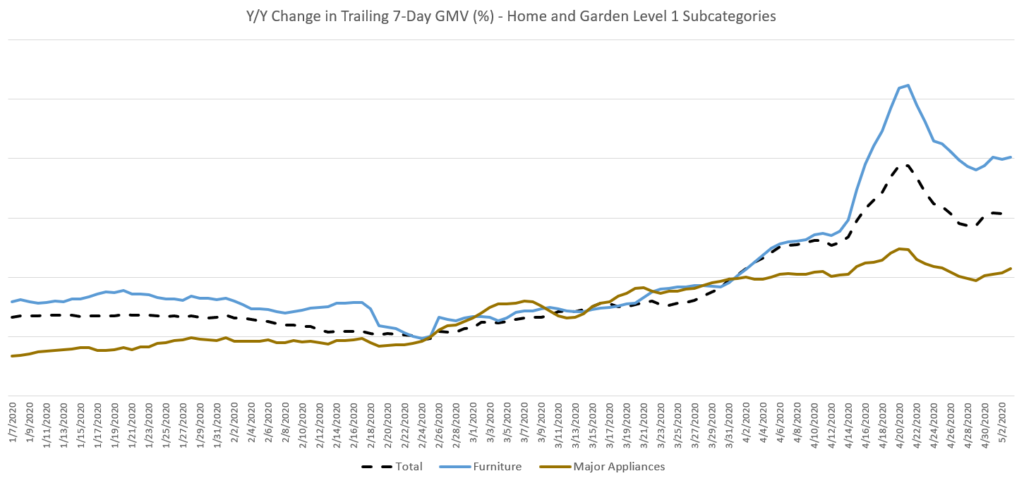

Furniture and Major Appliances

Growth in the L1Cats of “furniture” and “major appliances” tracked closely with the overall “home and garden” category until April, when the overall category started growing much faster than purchases of appliances. Sales growth of major appliances certainly didn’t decline, however. As we have reviewed in prior posts, it’s just that necessities for the consumers’ new work-from-home environments grew even faster. One example from prior posts is the subcategory of desks and home office furniture, which was a major contributor to the increased growth seen below in the furniture L1Cat.

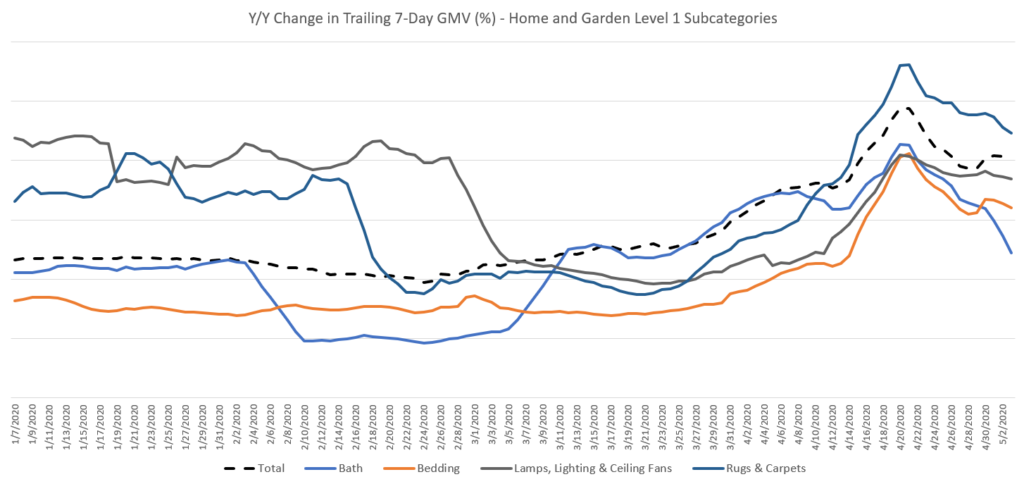

Non-Essential Home & Garden

The final L1Cats below would be considered discretionary purchases, for the most part. All of these L1Cats except “bedding” experienced a decline in year-over-year growth rates in February. And all of them grew at the same trajectory as the overall category from March into the stimulus bump. Only the L1Cat “lamps, lighting and ceiling fans” entered early May with growth rates below those of earlier in 2020.

Conclusion

The stimulus bump may (or may not?) be over, though we have continued to see growth rates in many categories that are higher than they were earlier in 2020. It may be too early to say for sure how much of this growth is due to the stimulus payments or the overall growth in e-commerce as a result of people remaining at home and avoiding retail stores (many of which remain closed). It’s also too early to determine whether we’ll see a permanent shift in incremental e-commerce adoption even as economies open back up and things return to normal. We will continue to follow these trends and provide analysis as the story continues.

In closing, we would like to reiterate from our original blog post that the COVID-19 pandemic has created extreme turmoil globally. The impact on supply and demand and the way people work is in the news daily and can be seen in the data above. The impact seems trivial relative to the personal toll. Nevertheless, the job of ensuring that food, medicine, and other essentials make their way to people globally is important to keep society functioning as normally as possible while we work our way through the current pandemic. So, in addition to thanking medical professionals, researchers, and others for their heroic efforts in treating the sick and trying to find a cure, we’d like to thank those of you in the factories, in the grocery stores, in the distribution centers, and in the delivery trucks helping to bring us the items we need to live.