As all of us strive to make sense of and adjust to the COVID-19 pandemic, there has been a lot of talk in the news of hoarding, empty shelves, and more generally, an imbalance between supply and demand that we normally don’t consider a possibility. As we get past this — which we no doubt will, however long it takes — there are undoubtedly many lessons that will be learned and adjustments made by businesses, government, and all of us as individuals. But, in the here and now, Rithum aggregate GMV data highlights trends that are playing out in the news.

First, some caveats before digging into the data:

- This data is based on marketplaces gross merchandise value (GMV), aggregated across our entire customer base globally and compares Jan 1 – Mar 17, 2019, against Jan 1 – Mar 17, 2020.

- The data presented below highlights only specific marketplace categories, which are merely a subset of all categories. Because marketplaces have different category structures, the data is presented using categories that have been standardised by Rithum.

- This data is not a proxy for overall e-commerce activity or the performance of any individual business, including Rithum or any individual marketplace.

- The data shown below is based on a year-over-year comparison of trailing 7-day GMV and is expressed as percentage growth, but with actual numbers removed. The Y-axis scale is different on each graph.

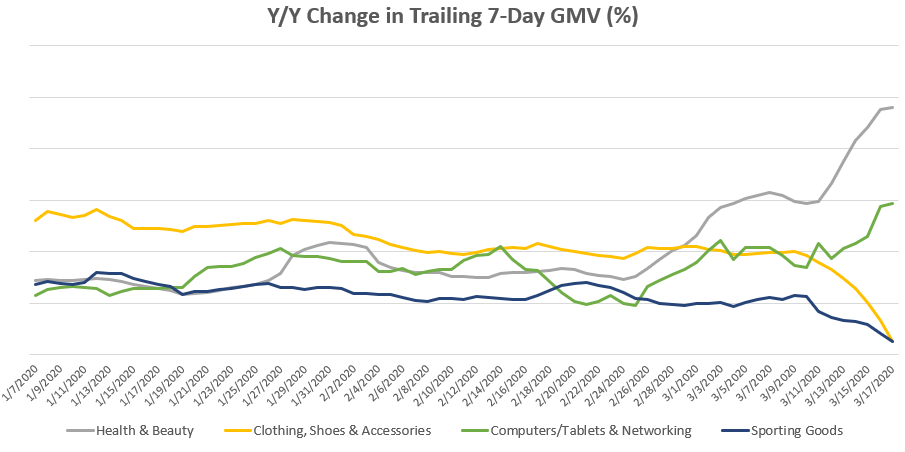

Broad Categories

It is hard to get a real sense of consumer demand using top-level categories. Nevertheless, a quick look at a handful of categories indicates that year-over-year GMV growth rates have increased recently in the health and beauty and computers/networking categories and have declined recently in apparel and sporting goods. We believe that this reflects increasing consumer focus on basic necessities and an adjustment to working from home (we will highlight this trend in other categories later).

Health & Beauty Category

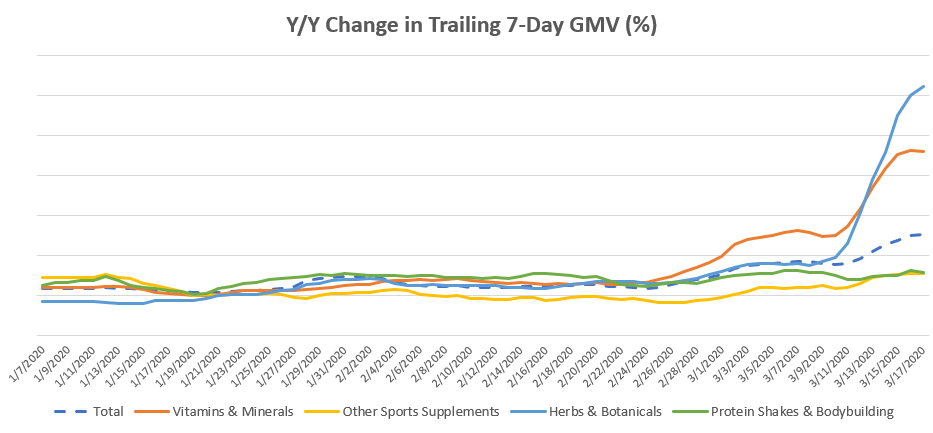

In our classification, we have more than 300 subcategories in the health and beauty segment. The chart below highlights several of the larger subcategories. As with the broader categories, we see here a trend with much stronger growth in the subcategories consumers see as essential: vitamins/minerals and herbs/botanicals. The other subcategories highlighted here related to sports supplements and bodybuilding are doing fine but have been relatively less important to consumers over the last month than basic vitamins and herbs.

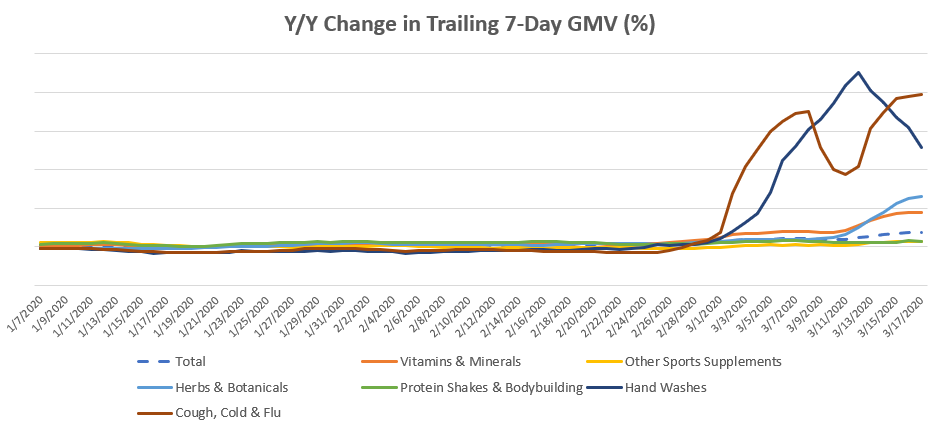

When we add in the “hand washes” and “cough, cold, flu” subcategories, it is evident that these are even more top of mind for consumers, leading to significant year-over-year growth (to be clear, these subcategories are smaller overall than the ones previously discussed).

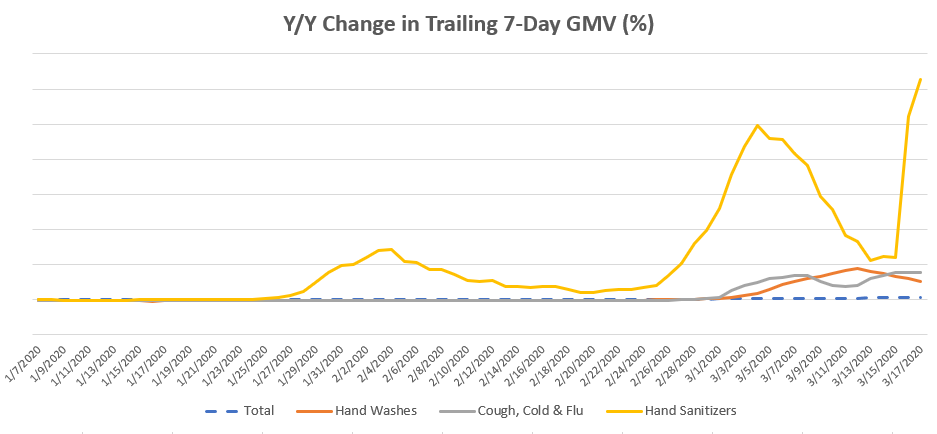

Finally, with hand sanitisers in the news, let’s see how this subcategory stacks up to the fast-growing “hand washes” and “cough, cold, flu” subcategories from the previous chart. The relative growth rate speaks for itself. Personally, I can’t find hand sanitiser in local stores. It appears consumers are going online for this instead.

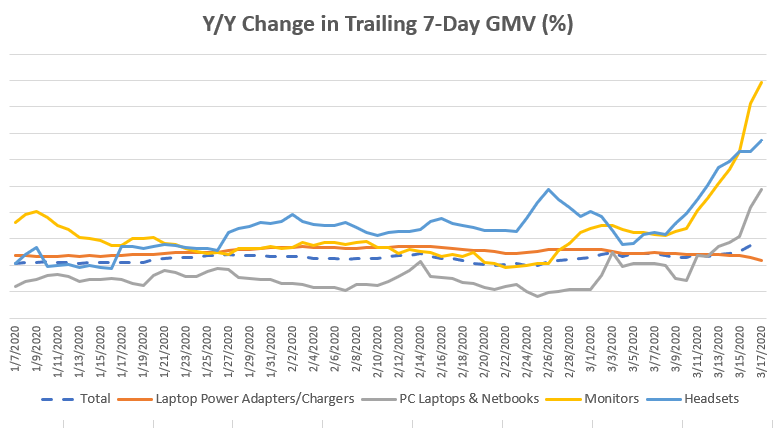

Computers, Tablets, and Networking Category

The growth in this category appears to be led by monitors, followed by laptops and notebooks. As we see in other categories, these trends are likely heavily influenced by the large numbers of businesses that are encouraging their employees to work from home. Growth in the headset subcategory also supports this hypothesis.

Home and Garden

The home and garden category wasn’t highlighted in the initial chart. On the surface, the category has steady year-over-year growth, with some puts and takes over the course of the first quarter to date. However, when you look deeper at specific subcategories, you can see the influence of recent events.

The broad home and garden category has more than 1,000 subcategories, with GMV well diversified across many of those subcategories. While the subcategories are too numerous to comment on individually, we have seen weakness relative to overall performance over the last 7 to 10 days in subcategories that could be considered discretionary, including lamps, area rugs, wall fixtures, and wheelbarrows, among others. It is too early to say if this will be a temporary blip or something longer lasting.

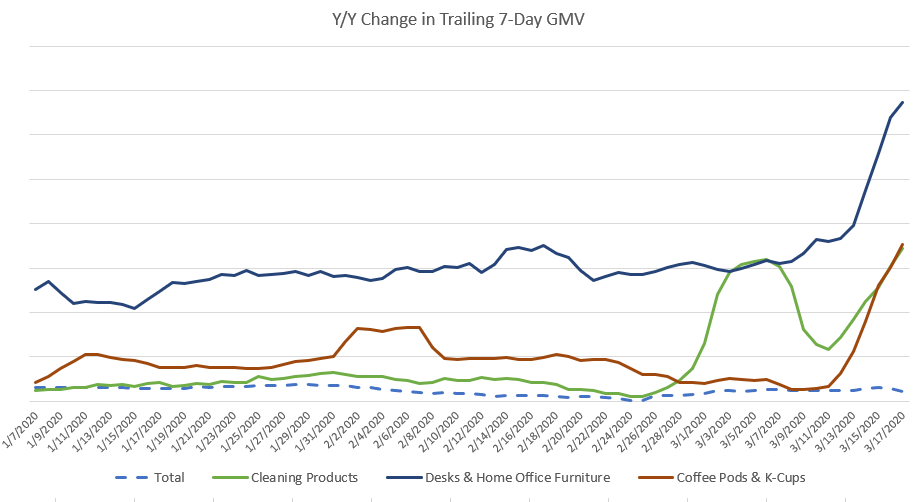

Meanwhile, there has been explosive growth in subcategories that relate to preparation for the COVID-19 virus (cleaning products) and working from home (office furniture and coffee pods), as illustrated below.

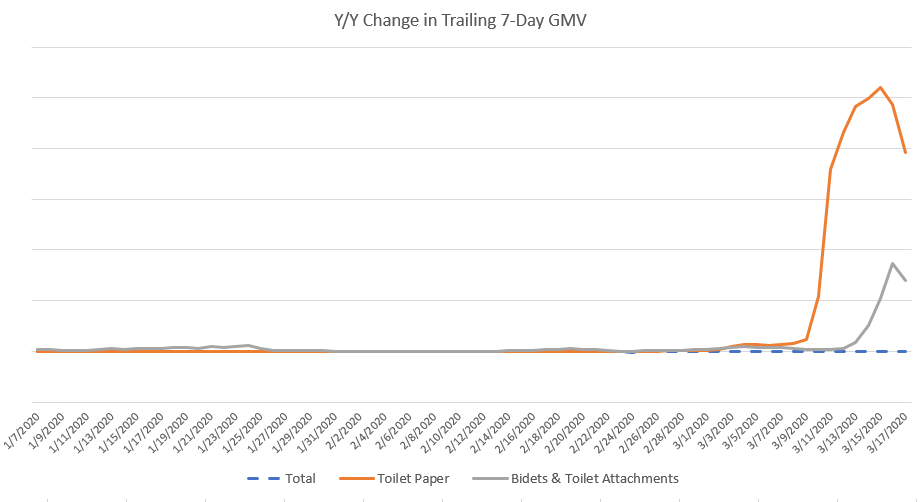

Finally, anyone that has attempted to get toilet paper at the local grocery store understands the growth in the subcategories highlighted below. I suspect the downward trend in toilet paper over the last several days is driven more by supply issues than a reduction in demand. The good news, however, is that experts predict this problem will soon be in the past.

Business and Industrial

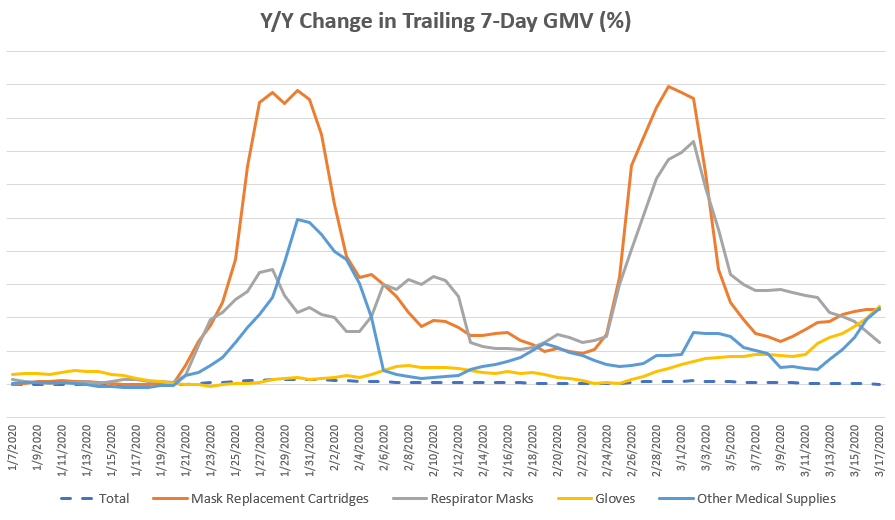

Business and Industrial is another very broad category, with more than 1,200 subcategories. As with Home and Garden, we focus on just a handful of subcategories to illustrate trends related to the COVID-19 pandemic. The “Total” line, though not flat during this time period, looks flat due to the high year-over-year growth rates in the subcategories pictured.

Conclusion

The COVID-19 pandemic has created extreme turmoil globally. The impact on supply and demand and the way people work is in the news daily and can be seen in the data above. The impact seems trivial relative to the personal toll. Nevertheless, the job of ensuring that food, medicine, and other essentials make their way to people globally is important to keep society functioning as normally as possible while we work our way through the current pandemic. So, in addition to thanking medical professionals, researchers, and others for their heroic efforts in treating the sick and trying to find a cure, we’d like to thank those of you in the factories, in the grocery stores, in the distribution centers, and in the delivery trucks helping to bring us the items we need to live.